Tragedy: IUL Lawsuits – A Growing Risk for You?

The problem is bigger than you think. There’s even the potential to capture the attention of Congress. After all, life insurance is life insurance – first.

Some recollect the 1993 lawsuit involving nurses in Florida. It’s one reason we added “insurance” in our positioning when life insurance is used to supplement retirement income.

The sharks are circling. With Indexed UL, attorneys have latched on to producer’s alleged misrepresentations using the sales application, “life insurance retirement plans.” This resulted in plaintiffs targeting IUL products that have high charge structures and high-risk reward tradeoffs (some with high dialable commissions).

Now, had these policies performed fine, we would all be fine. Fine without fearing the risk of a slippery slope cascading to other products. But still, here we are…

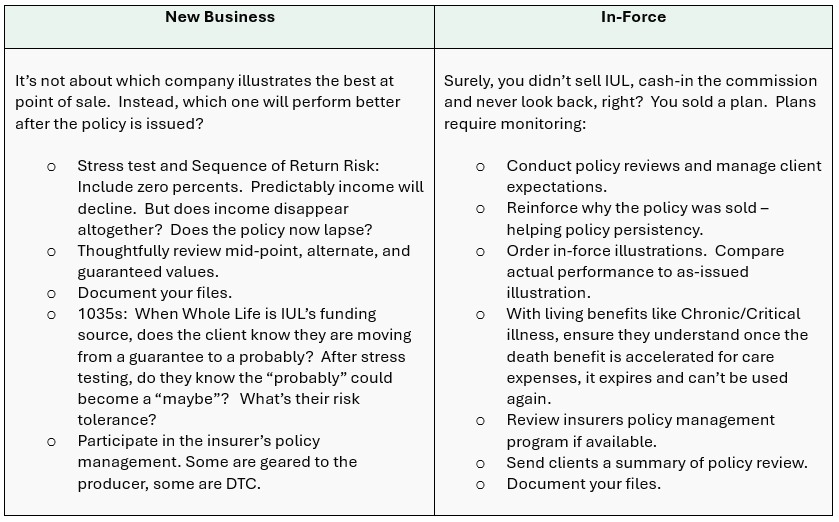

Illustrations

There’s an obsession to benchmark life products. Press calculate; which company wins? The product with the lowest premium or highest income often gets the sale with far less attention to other metrics like financial strength, service, or product features. For the winners it translates into hundreds of millions of dollars in additional premiums.

During the IUL arms race, AG-49 iterations were instrumental in leveling the playing field for comparing illustrations by establishing guard rails for maximum interest rates. They helped manage client expectations highlighting a range of outcomes with midpoint/alternative values.

Unfortunately, our history of in-fighting during these public meetings has backfired. Today they are used as a blueprint by plaintiffs as evidence for context and motive.

Warning

Litigants aren’t just targeting the deepest pockets – the insurers. Jurys have ordered both insurers and producers to pay out millions in IUL retirement loss cases.

Additionally, you should know that there’s the potential for you to be left standing alone. Insurers are sometimes successful in getting themselves dismissed from the lawsuit.

And another thing. For those of you into premium financing… Sigh. Be careful in your client selection and please tell me you aren’t focused on the middle market. Premium financing lawsuits are more common and any under performance is exposed earlier. BTW, when was the last time you looked at your E/O policy? Is there an exclusion for claims arising from premium-financed policies?

If so, you may indeed be left standing alone. Facing the entire liability.

Schadenfreude

Those IUL’s with more conservative product structures and illustration assumptions missed out on millions… Understandably, it may be tempting for them to gloat. The same could be said for Whole Life carriers – who for decades watched their guaranteed products traded in for cheaper ULs/VULs/IULs. But hold on. This isn’t really about IUL or AG-49.

The heart of the lawsuits is that life insurance was mis-sold as retirement income without regard to varying outcomes. That’s our problem and slippery slope.

Moving forward, can anyone, disappointed with their cash accumulation, turn against the producer and therefore the insurer, alleging the same? (Consider that technically, most policies haven’t had time to perform yet, since it’s too soon for income).

While certain IULs are easier to target, lawsuits could also be brought against VULs and Whole Life. (Albeit less likely. Whole life for obvious reasons. VUL’s due to who the sellers and buyers are).

Congress

Life insurance enjoys income tax free cash value growth, transfers between accounts, distributions, and death benefit. But Congress didn’t afford these privileges, so the rich could get richer. They did so for widows and orphans, to prevent them from being on welfare.

Do you remember how in 1988, Congress had to intervene? The rich were slapped with TAMRA highlighting new MEC rules. A reminder – that life insurance is not a tax shelter nor an investment (although my gosh, it still works nicely). Furthermore, you’ve probably noticed how in the early years of an illustration – you can’t withdraw to cost basis (instead, loans are forced). That was Uncle Sam with “recapture ceiling.” Again, same message. Life insurance is life insurance – first.

What You Can Do

As a producer, if you are alarmed, then stop falling into rabbit holes of IUL terms. Get back to basics. It would be like selling a car and focusing on heated seats – while never mentioning the need for an oil change or maintenance.

Policy Management

Sometimes with policy management programs one needs to proactively opt-in. They vary significantly. Some will automatically make adjustments in premium billings based on a targeted objective like cash value accumulation. Others may send notifications that it’s time to act, like switching death benefit options. Carriers may send a summary comparing the client’s overall policy performance to the as-issued illustration to communicate if it’s on track or not. Some may do this with a check-up to reflect if the policy is in the red, yellow, or green. You can find policy management related to:

- Automatic in-force illustrations – at policy anniversary

- Scheduled premiums vs. actual

- Policy performance – whether Accumulation or Protection focus – premiums may need to be adjusted to meet intended goal

- Notify it’s the planned time to start income

- Reduction in DB or 2/1 switch

- Status of guarantee (when applicable; critical for GULs)

- Income (managing either to a dollar amount or duration depending on performance)

- Status of Wellness benefits

- Digital platform for engaged producers to track and set alert notifications on client’s performance

Tragedy

Obviously, there are many IULs that have done well and better. These consumers are happy.

Still, the sharks are circling and there is blood in the water. Some producers, firms, and insurers have greater exposure than others. So far, we’ve seen the affluent hire legal counsel alleging harm. But what happens if it’s mom and pop? Like Edith and Archie with modest assets whose life insurance is their sole income strategy. Worse yet, at their age, it’s performing badly. (Precisely what would capture the attention of Congress).

Even if you are confident in our lobbyists and undisturbed with this risk… I ask you to recall Zuckerberg, or the Ivy League university presidents being grilled before Congress. They fumbled and stood frozen looking like a deer caught in headlights. Could this happen to our life insurance CEOs?

While there is rivalry between product categories and between insurers, we should circle the wagons.

If most of our life sales (collectively) are focused on income strategies for the wealthy, then perhaps we have lost our way. Our North Star of protection.

Have you lost your way? Do you manage client expectations at the point of sale and after policy issue?

We all know the good of life insurance. The middle class need death benefits to create generational wealth. Many were rescued by their cash values after the 2008 market crash. The tragedy would be any outcome that adversely impacts them – or the widows and orphans.

So, I leave you with the elementary. Regardless of the priority life insurance sales application. And regardless of the underlying product chassis.

Life insurance is life insurance. First. Don’t ever forget it.

You are responsible for your own due diligence. This information is not guaranteed for accuracy and is subject to change. This content should not be construed as rendering specific tax, insurance, investment, or legal advice. You acknowledge that any reliance on this material or any opinion, statement, or information is at your sole risk. If you take any action based on the information, you take full responsibility for the results of that action. You should independently verify its content.

Be the first to know